15. Inventory Management Model#

GPU

This lecture was built using a machine with JAX installed and access to a GPU.

To run this lecture on Google Colab, click on the “play” icon top right, select Colab, and set the runtime environment to include a GPU.

To run this lecture on your own machine, you need to install Google JAX.

This lecture provides a JAX implementation of a model in Dynamic Programming.

In addition to JAX and Anaconda, this lecture will need the following libraries:

!pip install --upgrade quantecon

Show code cell output

Requirement already satisfied: quantecon in /home/runner/miniconda3/envs/quantecon/lib/python3.13/site-packages (0.9.0)

Requirement already satisfied: numba>=0.49.0 in /home/runner/miniconda3/envs/quantecon/lib/python3.13/site-packages (from quantecon) (0.61.0)

Requirement already satisfied: numpy>=1.17.0 in /home/runner/miniconda3/envs/quantecon/lib/python3.13/site-packages (from quantecon) (2.1.3)

Requirement already satisfied: requests in /home/runner/miniconda3/envs/quantecon/lib/python3.13/site-packages (from quantecon) (2.32.3)

Requirement already satisfied: scipy>=1.5.0 in /home/runner/miniconda3/envs/quantecon/lib/python3.13/site-packages (from quantecon) (1.15.3)

Requirement already satisfied: sympy in /home/runner/miniconda3/envs/quantecon/lib/python3.13/site-packages (from quantecon) (1.13.3)

Requirement already satisfied: llvmlite<0.45,>=0.44.0dev0 in /home/runner/miniconda3/envs/quantecon/lib/python3.13/site-packages (from numba>=0.49.0->quantecon) (0.44.0)

Requirement already satisfied: charset-normalizer<4,>=2 in /home/runner/miniconda3/envs/quantecon/lib/python3.13/site-packages (from requests->quantecon) (3.3.2)

Requirement already satisfied: idna<4,>=2.5 in /home/runner/miniconda3/envs/quantecon/lib/python3.13/site-packages (from requests->quantecon) (3.7)

Requirement already satisfied: urllib3<3,>=1.21.1 in /home/runner/miniconda3/envs/quantecon/lib/python3.13/site-packages (from requests->quantecon) (2.3.0)

Requirement already satisfied: certifi>=2017.4.17 in /home/runner/miniconda3/envs/quantecon/lib/python3.13/site-packages (from requests->quantecon) (2025.4.26)

Requirement already satisfied: mpmath<1.4,>=1.1.0 in /home/runner/miniconda3/envs/quantecon/lib/python3.13/site-packages (from sympy->quantecon) (1.3.0)

15.1. A model with constant discounting#

We study a firm where a manager tries to maximize shareholder value.

To simplify the problem, we assume that the firm only sells one product.

Letting

Suppose the firm faces exogenous demand process

We assume

Inventory

The term

We assume that the firm can store at most

Profits are given by

We take the minimum of current stock and demand because orders in excess of inventory are assumed to be lost rather than back-filled.

Here

We can map our inventory problem into a dynamic program with state space

The feasible correspondence

which represents the set of feasible orders when the current inventory

state is

The reward function is expected current profits, or

The stochastic kernel (i.e., state-transition probabilities) from the set of feasible state-action pairs is

When discounting is constant, the Bellman equation takes the form

15.2. Time varing discount rates#

We wish to consider a more sophisticated model with time-varying discounting.

This time variation accommodates non-constant interest rates.

To this end, we replace the constant

We suppose that the dynamics can be expressed as

After relabeling inventory

where

We set

Now

Hence we can rewrite (15.2) as

Let’s begin with the following imports

import quantecon as qe

import jax

import jax.numpy as jnp

import numpy as np

import matplotlib.pyplot as plt

from time import time

from functools import partial

from typing import NamedTuple

Let’s check the GPU we are running

!nvidia-smi

Mon Aug 25 03:36:10 2025

+-----------------------------------------------------------------------------------------+

| NVIDIA-SMI 575.51.03 Driver Version: 575.51.03 CUDA Version: 12.9 |

|-----------------------------------------+------------------------+----------------------+

| GPU Name Persistence-M | Bus-Id Disp.A | Volatile Uncorr. ECC |

| Fan Temp Perf Pwr:Usage/Cap | Memory-Usage | GPU-Util Compute M. |

| | | MIG M. |

|=========================================+========================+======================|

| 0 Tesla T4 Off | 00000000:00:1E.0 Off | 0 |

| N/A 37C P8 9W / 70W | 0MiB / 15360MiB | 0% Default |

| | | N/A |

+-----------------------------------------+------------------------+----------------------+

+-----------------------------------------------------------------------------------------+

| Processes: |

| GPU GI CI PID Type Process name GPU Memory |

| ID ID Usage |

|=========================================================================================|

| No running processes found |

+-----------------------------------------------------------------------------------------+

We will use 64 bit floats with JAX in order to increase the precision.

jax.config.update("jax_enable_x64", True)

Let’s define a model to represent the inventory management.

# NamedTuple Model

class Model(NamedTuple):

z_values: jnp.ndarray # Exogenous shock values

Q: jnp.ndarray # Exogenous shock probabilities

x_values: jnp.ndarray # Inventory values

d_values: jnp.ndarray # Demand values for summation

ϕ_values: jnp.ndarray # Demand probabilities

p: float # Demand parameter

c: float = 0.2 # Unit cost

κ: float = 0.8 # Fixed cost

def create_sdd_inventory_model(

ρ: float = 0.98, # Exogenous state autocorrelation parameter

ν: float = 0.002, # Exogenous state volatility parameter

n_z: int = 10, # Exogenous state discretization size

b: float = 0.97, # Exogenous state offset

K: int = 100, # Max inventory

D_MAX: int = 101, # Demand upper bound for summation

p: float = 0.6

) -> Model:

# Demand

def demand_pdf(p, d):

return (1 - p)**d * p

d_values = jnp.arange(D_MAX)

ϕ_values = demand_pdf(p, d_values)

# Exogenous state process

mc = qe.tauchen(n_z, ρ, ν)

z_values, Q = map(jnp.array, (mc.state_values + b, mc.P))

# Endogenous state

x_values = jnp.arange(K + 1) # 0, 1, ..., K

return Model(

z_values=z_values, Q=Q,

x_values=x_values, d_values=d_values, ϕ_values=ϕ_values,

p=p

)

Here’s the function B on the right-hand side of the Bellman equation.

@jax.jit

def B(x, z_idx, v, model):

"""

Take z_idx and convert it to z. Then compute

B(x, z, a, v) = r(x, a) + β(z) Σ_x′ v(x′) P(x, a, x′)

for all possible choices of a.

"""

z_values, Q, x_values, d_values, ϕ_values, p, c, κ = model

z = z_values[z_idx]

def _B(a):

"""

Returns r(x, a) + β(z) Σ_x′ v(x′) P(x, a, x′) for each a.

"""

revenue = jnp.sum(jnp.minimum(x, d_values) * ϕ_values)

profit = revenue - c * a - κ * (a > 0)

v_R = jnp.sum(v[jnp.maximum(x - d_values, 0) + a].T * ϕ_values, axis=1)

cv = jnp.sum(v_R * Q[z_idx])

return profit + z * cv

a_values = x_values # Set of possible order sizes

B_values = jax.vmap(_B)(a_values)

max_x = len(x_values) - 1

return jnp.where(a_values <= max_x - x, B_values, -jnp.inf)

We need to vectorize this function so that we can use it efficiently in JAX.

We apply a sequence of vmap operations to vectorize appropriately in each

argument.

B = jax.vmap(B, in_axes=(None, 0, None, None))

B = jax.vmap(B, in_axes=(0, None, None, None))

Next we define the Bellman operator.

@jax.jit

def T(v, model):

"""The Bellman operator."""

z_values, Q, x_values, d_values, ϕ_values, p, c, κ = model

z_indices = jnp.arange(len(z_values))

res = B(x_values, z_indices, v, model)

return jnp.max(res, axis=2)

The following function computes a v-greedy policy.

@jax.jit

def get_greedy(v, model):

"""Get a v-greedy policy. Returns a zero-based array."""

z_values, Q, x_values, d_values, ϕ_values, p, c, κ = model

z_indices = jnp.arange(len(z_values))

res = B(x_values, z_indices, v, model)

return jnp.argmax(res, axis=2)

Here’s code to solve the model using value function iteration.

@jax.jit

def solve_inventory_model(v_init, model, max_iter=10_000, tol=1e-6):

"""Use successive_approx to get v_star and then compute greedy."""

def update(state):

error, i, v = state

new_v = T(v, model)

new_error = jnp.max(jnp.abs(new_v - v))

new_i = i + 1

return new_error, new_i, new_v

def test(state):

error, i, v = state

return (i < max_iter) & (error > tol)

i, error = 0, tol + 1

initial_state = error, i, v_init

final_state = jax.lax.while_loop(test, update, initial_state)

error, i, v_star = final_state

σ_star = get_greedy(v_star, model)

return v_star, σ_star

Now let’s create an instance and solve it.

model = create_sdd_inventory_model()

z_values, Q, x_values, d_values, ϕ_values, p, c, κ = model

n_z = len(z_values)

n_x = len(x_values)

v_init = jnp.zeros((n_x, n_z), dtype=float)

start = time()

v_star, σ_star = solve_inventory_model(v_init, model)

# Pause until execution finishes

jax.tree_util.tree_map(lambda x: x.block_until_ready(), (v_star, σ_star))

jax_time_with_compile = time() - start

print(f"compile plus execution time = {jax_time_with_compile * 1000:.6f} ms")

compile plus execution time = 1429.393530 ms

Let’s run again to get rid of the compile time.

start = time()

v_star, σ_star = solve_inventory_model(v_init, model)

# Pause until execution finishes

jax.tree_util.tree_map(lambda x: x.block_until_ready(), (v_star, σ_star))

jax_time_without_compile = time() - start

print(f"execution time = {jax_time_without_compile * 1000:.6f} ms")

execution time = 819.420576 ms

Now let’s do a simulation.

We’ll begin by converting back to NumPy arrays for convenience

Q = np.array(Q)

z_values = np.array(z_values)

z_mc = qe.MarkovChain(Q, z_values)

Here’s code to simulate inventories

def sim_inventories(ts_length, X_init=0):

"""Simulate given the optimal policy."""

global p, z_mc

z_idx = z_mc.simulate_indices(ts_length, init=1)

X = np.zeros(ts_length, dtype=np.int32)

X[0] = X_init

rand = np.random.default_rng().geometric(p=p, size=ts_length-1) - 1

for t in range(ts_length-1):

X[t+1] = np.maximum(X[t] - rand[t], 0) + σ_star[X[t], z_idx[t]]

return X, z_values[z_idx]

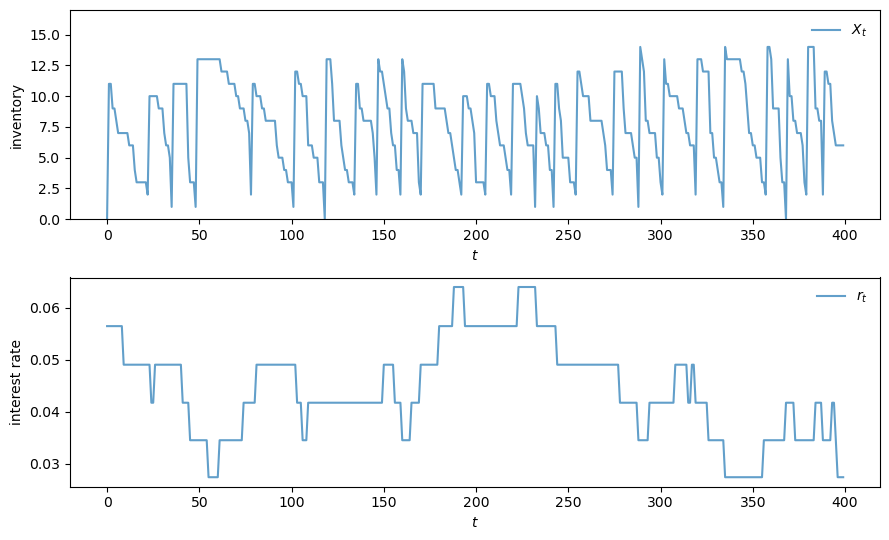

Here’s code to generate a plot.

def plot_ts(ts_length=400, fontsize=10):

X, Z = sim_inventories(ts_length)

fig, axes = plt.subplots(2, 1, figsize=(9, 5.5))

ax = axes[0]

ax.plot(X, label=r"$X_t$", alpha=0.7)

ax.set_xlabel(r"$t$", fontsize=fontsize)

ax.set_ylabel("inventory", fontsize=fontsize)

ax.legend(fontsize=fontsize, frameon=False)

ax.set_ylim(0, np.max(X)+3)

# calculate interest rate from discount factors

r = (1 / Z) - 1

ax = axes[1]

ax.plot(r, label=r"$r_t$", alpha=0.7)

ax.set_xlabel(r"$t$", fontsize=fontsize)

ax.set_ylabel("interest rate", fontsize=fontsize)

ax.legend(fontsize=fontsize, frameon=False)

plt.tight_layout()

plt.show()

Let’s take a look.

plot_ts()